Introduction

Many people assume budgeting is about restricting what you can spend. In reality, a personal budget is a tool for clarity and control. It helps you understand where your money comes from, where it goes, and whether your spending aligns with what matters to you. For UK residents, this becomes particularly relevant given the combination of council tax, National Insurance, rent or mortgage payments, and varying utility costs. This guide walks you through building a practical, sustainable budget from absolute zero – no special software required, just basic maths and honesty about your habits.

Based on rules as of August 2025. Always verify current rates with official sources.

Why Budgeting Matters for UK Households

The cost of living in the United Kingdom varies significantly by region, but certain expenses affect everyone: council tax bands, water bills, energy costs, and television licences. Without a budget, it is easy to underestimate monthly outgoings or forget annual expenses like car insurance or home maintenance. A budget also reveals whether you are saving enough for short-term goals (a holiday, a new car) or long-term ones (a house deposit, retirement). Perhaps most importantly, a budget reduces financial anxiety. When you know exactly how much you can spend on groceries or socialising, guilt-free spending becomes possible.

Step 1: Calculate Your After-Tax Income

Your starting point is your take-home pay – the amount that actually lands in your bank account each month. If you are employed, look at your payslip and find the figure labelled “Net Pay” or “Take Home Pay”. This already accounts for Income Tax, National Insurance, and any pension contributions. If you have variable income (freelance, zero-hours contract, commission-based), calculate a conservative average using the last three to six months. Include any other reliable income sources: child benefit, maintenance payments, regular bank interest, or dividends from investments.

Do not include overtime or bonuses unless they are guaranteed. It is safer to treat extra income as a surplus to be saved or used for one-off treats.

Step 2: List Everything You Spend Money On

This step requires honesty. Gather three months of bank statements and go through every transaction. Divide your spending into two categories:

Fixed costs (essential and predictable):

- Rent or mortgage

- Council tax

- Gas and electricity

- Water bill

- Home and car insurance

- TV licence and broadband

- Mobile phone contract

- Minimum debt repayments (credit cards, loans)

- Childcare or school costs

Variable costs (change month to month):

- Groceries

- Transport (fuel, public transport, parking)

- Eating out and takeaways

- Clothing and personal care

- Gifts and celebrations

- Subscriptions (streaming, gym, magazines)

- Hobbies and entertainment

Do not forget annual or quarterly expenses. Divide them by 12 to get a monthly equivalent. Examples include car tax, MOT, service charges, professional memberships, and Christmas presents.

Step 3: Choose a Budgeting Method That Works for You

There is no single correct way to budget. Three popular approaches work well for UK households:

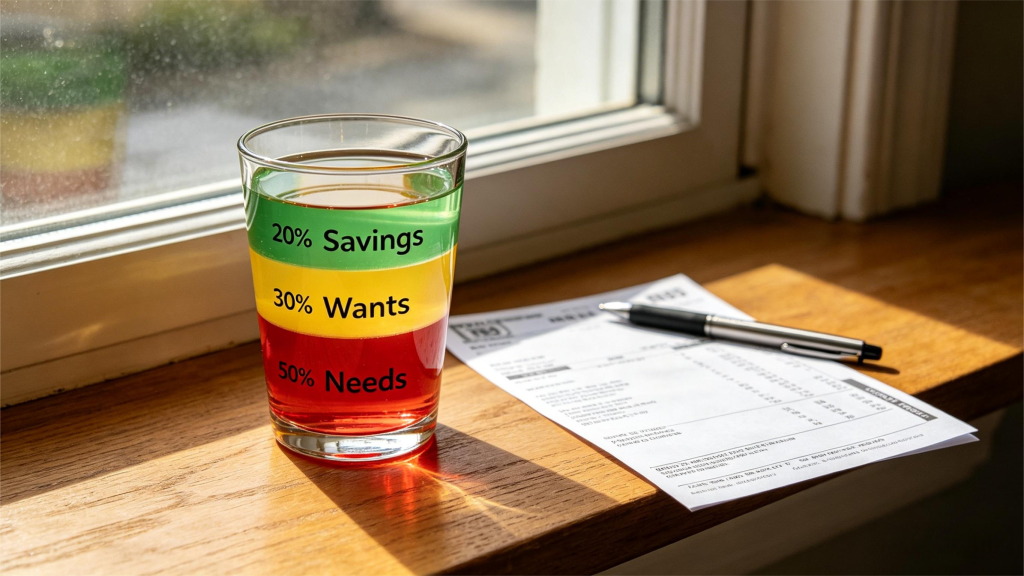

The 50/30/20 rule: Allocate 50% of your after-tax income to needs (rent, bills, groceries), 30% to wants (eating out, hobbies, subscriptions), and 20% to savings and debt overpayments. This works well for people with stable incomes and moderate housing costs.

Zero-based budgeting: Assign every pound a job. Income minus outgoings should equal zero. This method requires tracking every transaction but gives maximum control.

Envelope budgeting: Withdraw cash for variable categories (groceries, entertainment, transport) and put each category’s budget into a separate envelope. When an envelope is empty, you stop spending in that category. Many people now do this digitally using budgeting apps that create virtual envelopes.

For beginners, the 50/30/20 rule is often the easiest starting point. You can refine it after three months.

Step 4: Compare Income and Outgoings

Subtract your total monthly spending from your net monthly income. If the result is positive, you have a surplus that can go toward savings, investments, or debt reduction. If the result is negative, you are spending more than you earn – which typically leads to growing debt or dipping into savings.

Do not panic if you are in negative territory. The budget has done its job by revealing the problem. Now you can decide where to cut back. Common first adjustments include:

- Reducing takeaways or restaurant meals

- Switching to a cheaper mobile or broadband provider

- Canceling unused subscriptions

- Using a food shopping list to avoid impulse buys

- Walking or cycling shorter journeys instead of driving

Small changes add up. Saving £5 per day on coffee and lunch amounts to over £1,800 per year.

Step 5: Build Your Budget and Track It

Write your budget down. Use a spreadsheet, a notebook, or a free budgeting app (many UK banks now offer spending categorisation within their own apps). The format matters less than consistency.

Set a regular time each week to review transactions. On a Sunday evening, spend ten minutes entering the week’s spending and comparing it to your budget. If you overspent in one category, reduce another category to balance it. If you underspend, move the surplus to savings.

At the end of each month, do a fuller review. Ask yourself three questions:

- Did I stick to my budget overall?

- Which categories were consistently over or under?

- Do I need to adjust my budget (e.g., I underestimated grocery costs)?

Adjust as needed. A budget is a living document, not a punishment.

Key Takeaways

- Start with after-tax income – never budget based on gross salary.

- Separate fixed from variable costs – fixed costs are harder to change quickly.

- Choose one budgeting method – 50/30/20 is excellent for beginners.

- Track weekly, review monthly – consistency beats intensity.

- Be honest and flexible – a budget that ignores reality will fail.

This article is for general information and educational purposes only. It does not constitute financial advice. Tax rules, allowances, and product terms may change. Always check with HMRC or an FCA-authorised adviser for your personal circumstances.