Introduction

A year-end bonus, a tax refund, an unexpected gift, or overtime pay – these windfalls can transform your finances if allocated deliberately. Too often, people treat extra income as “fun money” and spend it on indulgences that provide fleeting satisfaction. A smarter approach recognises that a windfall is an opportunity to accelerate your financial goals: paying down debt, building an emergency fund, investing for the future, or treating yourself without guilt. This guide provides a framework for allocating any amount of extra income, from £100 to £10,000 or more.

Based on rules as of November 2025. Always verify current rates with official sources.

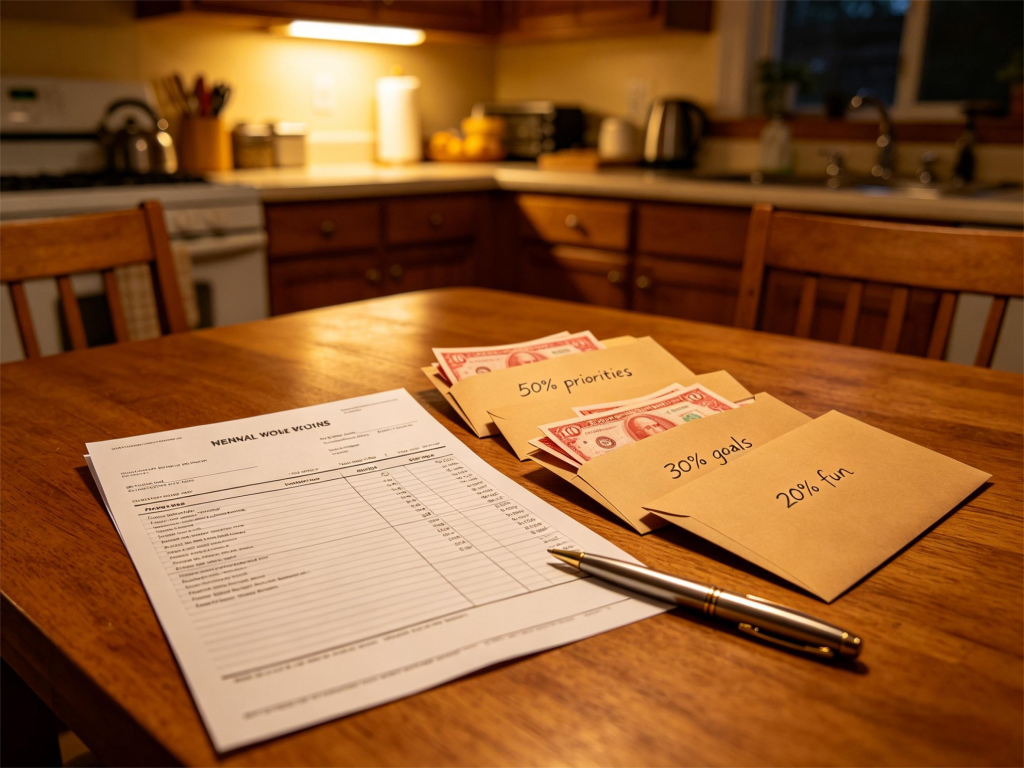

The 50/30/20 Rule for Windfalls (Modified)

The standard 50/30/20 budget (needs/wants/savings) works well for regular income. For windfalls, a modified version is more appropriate:

- 50% toward financial priorities – debt reduction, emergency fund, retirement savings.

- 30% toward near-term goals – house deposit, holiday fund, home improvement, car replacement.

- 20% for guilt-free spending – something you genuinely enjoy (restaurant, weekend away, hobby equipment).

This framework ensures that most of your windfall improves your financial position, while still allowing some enjoyment. The exact percentages can shift based on your situation. If you have high-cost debt, consider 70/20/10 or even 100/0/0 until the debt is gone.

Step 1: Assess Your Financial Foundation

Before allocating any windfall, check your foundation. If any of these are missing, prioritise them first – even before debt repayment (except high-cost debt).

Priority 1: High-cost debt elimination. Credit cards with interest above 15%, overdrafts, payday loans. These debts cost more than most investments earn. Pay them off immediately.

Priority 2: Emergency fund. If you have less than one month of essential expenses saved, use your windfall to build that buffer. Without an emergency fund, any unexpected cost (car repair, boiler breakdown) pushes you back into debt.

Priority 3: Essential bills arrears. Council tax, utility bills, rent/mortgage arrears. These have serious consequences (court action, eviction, repossession). Clear them before any discretionary allocation.

Once your foundation is solid, you can allocate the windfall across the three categories below.

Allocation Option 1: Pay Down Debt (High Impact)

Debt repayment is often the highest-return use of a windfall. Every pound you use to pay off a debt with 20% APR is effectively earning a 20% risk-free return – because you no longer pay that interest.

Which debt to target first:

- Highest interest rate first (debt avalanche) – Mathematically optimal. List debts by APR, pay minimums on all, put the windfall toward the highest APR debt.

- Smallest balance first (debt snowball) – Psychologically motivating. Pay off the smallest debt completely, giving you a sense of progress. Studies suggest this method leads to higher success rates for some people.

Example: You have a credit card with £2,000 at 22% APR and a personal loan with £5,000 at 8% APR. A £1,000 windfall should go entirely to the credit card under either method (highest rate or smallest balance).

What about 0% credit cards? If you have a 0% purchase or balance transfer card, do not overpay it early. Put the windfall into a savings account earning interest, then pay the credit card just before the 0% period ends. This is called “stoozing” – but only if you are disciplined.

Allocation Option 2: Boost Your Emergency Fund

A fully funded emergency fund (3–6 months of essential expenses) is a form of self-insurance. Without it, you are one car breakdown or boiler failure away from high-cost debt.

Use a windfall to:

- Move from 1 month to 3 months of expenses.

- Move from 3 months to 6 months if you have unstable income (freelance, commission-based, seasonal work).

- Top up after a year when you used the emergency fund (e.g., you had a large car repair).

Keep your emergency fund in easy access cash (savings account or Cash ISA). Do not invest it – investments can fall just when you need the money.

Allocation Option 3: Invest for Long-Term Growth

If your foundation is solid and you have no high-cost debt, investing a windfall can generate significant long-term returns.

Pension contributions – A windfall paid into your pension receives tax relief at your marginal rate. A basic-rate taxpayer contributing £1,000 actually gets £1,250 in their pension (the government adds £250). A higher-rate taxpayer can claim additional relief, making a £1,000 contribution cost as little as £600 after tax relief (depending on how you contribute).

Stocks and Shares ISA – If you have not used your annual ISA allowance, contributing a windfall to a Stocks and Shares ISA protects all future growth and income from tax.

Lifetime ISA – If you are a first-time buyer or saving for retirement, a LISA adds a 25% government bonus on contributions up to £4,000 per tax year. A £4,000 windfall becomes £5,000 instantly (plus any investment growth).

General investment account – If your ISA and pension allowances are fully used, you can invest in a general account. But be mindful of tax on dividends and capital gains.

Allocation Option 4: Near-Term Goals (1–5 Years)

Not every pound needs to be locked away for decades. A windfall can accelerate goals that improve your quality of life.

House deposit – If you are saving for a first home, a windfall boosts your deposit. Keep it in a Cash LISA (for the bonus) or a high-interest easy access account if you might buy within 12 months.

Home improvements – Energy efficiency upgrades (insulation, heat pump, solar panels) can reduce future bills. Some improvements also add value to your home.

Education or training – A course, certification, or degree that increases your earning potential can have a high return on investment.

Holiday or wedding – Allocating a portion of a windfall to a memorable experience is reasonable. Just do not let it crowd out more important priorities.

Allocation Option 5: Guilt-Free Spending (The 20% Rule)

Financial discipline that allows no joy is unlikely to be sustainable. Allocating 20% (or less) of a windfall to pure enjoyment can help you stay motivated.

Examples:

- A weekend away.

- A meal at a restaurant you have wanted to try.

- A new piece of technology or hobby equipment.

- A donation to a charity you care about (with Gift Aid, the charity receives more).

The key is intentionality. Decide on the spending amount before you receive the windfall, not after. Impulse spending tends to be less satisfying than planned treats.

Special Case: Large Windfalls (£10,000+)

For larger sums, avoid making immediate decisions. The psychological impact of a large windfall can lead to poor choices (buying an expensive car, lending money to friends, investing in a friend’s business idea).

Suggested process for large windfalls:

- Do nothing for 30 days. Park the money in an easy access savings account. Resist the urge to spend or invest immediately.

- Revisit your financial priorities. Write down your goals. Discuss with a partner if applicable.

- Allocate across the categories above – debt, emergency fund, investments, near-term goals, guilt-free spending.

- Consider professional advice – if the windfall is more than 50% of your annual income, a one-off meeting with a chartered financial planner (paid by the hour, not commission) can be worthwhile.

Avoid these common mistakes:

- Upgrading your lifestyle permanently (leasing a more expensive car, moving to a larger rental). Windfalls are one-off – do not commit to recurring expenses.

- Investing in something you do not understand (cryptocurrency, a friend’s startup, a “guaranteed return” scheme).

- Telling many people about the windfall. It can create uncomfortable expectations.

Tax Considerations for Bonuses

If your year-end bonus is paid through payroll, it is subject to Income Tax and National Insurance in the usual way. Your employer will deduct these before you receive the bonus.

Salary sacrifice: If your employer offers salary sacrifice, you can ask for your bonus to be paid directly into your pension. This avoids both Income Tax and NICs entirely (though you cannot access the money until retirement age).

Bonus sacrifice for high earners: If your bonus pushes you over a tax threshold (e.g., £100,000, where the Personal Allowance begins to taper), sacrificing the bonus into your pension can preserve your tax-free allowance.

Key Takeaways

- Prioritise high-cost debt first – paying 20% APR debt is a 20% risk-free return.

- Build your emergency fund – 3–6 months of essential expenses before investing.

- Use the 50/30/20 windfall rule – 50% to financial priorities, 30% to near-term goals, 20% guilt-free.

- For large windfalls, wait 30 days – avoid impulsive decisions.

- Consider tax-efficient options – pension salary sacrifice or ISA contributions.

This article is for general information and educational purposes only. It does not constitute financial advice. Tax rules, allowances, and product terms may change. Always check with HMRC or an FCA-authorised adviser for your personal circumstances.