Introduction

Credit scores are widely misunderstood. Many people believe there is a single, official “credit score” that lenders use. In reality, the UK has three main credit reference agencies (CRAs), each with its own scoring system. Lenders do not see your score – they see your full credit report and apply their own criteria. That said, your score from agencies like Experian, Equifax, and TransUnion is a useful indicator of how lenders might view you. This guide explains what actually affects your creditworthiness, how to check your reports for free, and practical steps to improve your standing over time.

Based on rules as of August 2025. Always verify current rates with official sources.

The Three Credit Reference Agencies

Unlike some countries with a single government-run credit bureau, the UK has three private CRAs:

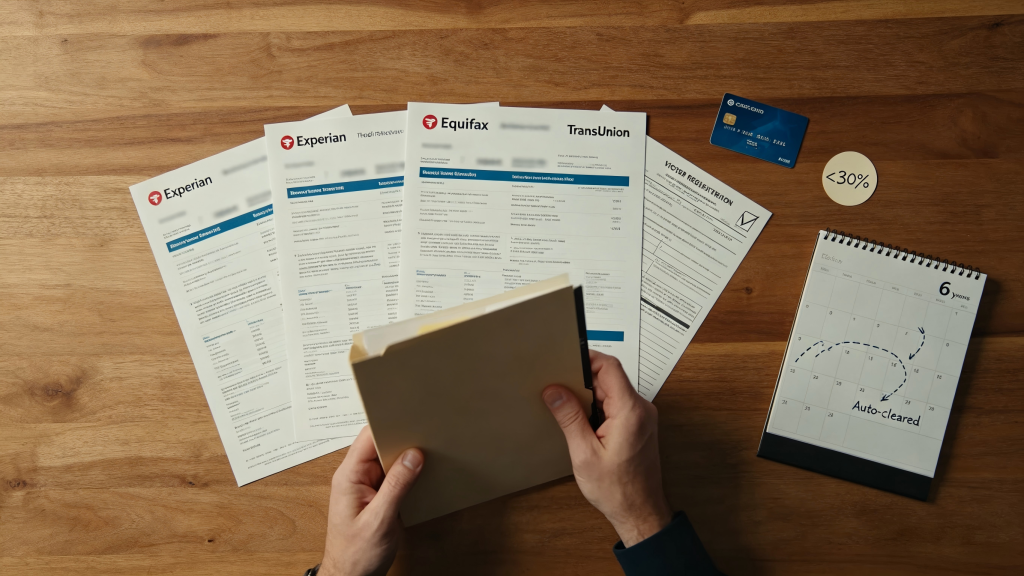

- Experian – scores range from 0 to 999. Many lenders use Experian.

- Equifax – scores range from 0 to 1,000. Also widely used.

- TransUnion – scores range from 0 to 710. Smaller but still significant.

Each agency holds slightly different information because not all lenders report to all three. A missed payment might appear on Equifax but not Experian, depending on which agency the lender uses. This is why checking all three reports is important.

Your score from each agency will differ. Do not panic if one is lower than another – focus on the underlying information, not the number.

What Actually Appears on Your Credit Report

Your credit report contains factual information about your financial behaviour. It includes:

Positive information:

- Electoral register registration (confirms your address)

- Credit accounts opened (credit cards, loans, mortgages)

- On-time repayment history

- Credit utilisation (how much of your available credit you use)

- Length of credit history

Negative information:

- Missed or late payments (stay for 6 years)

- Defaults (stay for 6 years)

- County Court Judgments (CCJs – stay for 6 years)

- Individual Voluntary Arrangements (IVAs – stay for 6 years)

- Bankruptcy (stay for 6 years)

- Hard searches (inquiries when you apply for credit – stay for 12 months)

What does NOT appear:

- Your salary (unless you tell a lender and they add a note)

- Savings account balances

- Student loan debt (student loans are not treated as normal credit)

- Council tax arrears (unless they go to court)

- Parking tickets (unless they go to court)

Factors That Affect Your Score (In Order of Importance)

Not all factors are equal. Based on how lenders typically weight information, here is what matters most:

1. Payment history (most important) – Have you paid previous credit on time? Even one missed payment can significantly lower your score for months.

2. Credit utilisation (very important) – This is the percentage of your available credit that you are using. Using more than 30% of your total credit limit (e.g., £3,000 on a £10,000 limit) is often seen as a warning sign. Using more than 90% is considered high risk.

3. Length of credit history – Older accounts are better. Closing your oldest credit card can shorten your average account age and lower your score.

4. Credit mix – Having a mix of credit types (credit card, loan, mortgage) is better than having only one type. But do not open accounts just to improve mix.

5. Recent credit applications – Multiple applications in a short period (e.g., 3+ in 6 months) suggests financial distress. Each application leaves a hard search.

6. Electoral registration – Being on the electoral roll at your current address confirms your identity and stability. Not being registered makes you harder to verify.

Common Myths About Credit Scores

Myth 1: Checking your own score lowers it. False. Checking your own report is a soft search, visible only to you. It has no effect on your score.

Myth 2: You have one universal credit score. False. Each CRA has its own score, and lenders use their own scoring models.

Myth 3: Closing unused credit cards improves your score. Often false. Closing a card reduces your available credit, which can increase your utilisation percentage and lower your score.

Myth 4: Having no credit means a perfect score. False. Lenders need evidence of responsible borrowing. No credit history makes you an unknown quantity, which many lenders treat as risky.

Myth 5: High income equals high credit score. False. Income is not on your credit report. Someone earning £30,000 with perfect payments can have a higher score than someone earning £200,000 with missed payments.

How to Check Your Credit Reports for Free

You are entitled to view your statutory credit report from each agency for free. However, many free services now offer ongoing access:

- Experian – CreditExpert offers a free 30-day trial, but the statutory report is free via their website.

- Equifax – ClearScore offers free ongoing access (funded by advertising).

- TransUnion – Credit Karma offers free ongoing access.

Check at least one report every three months. Stagger your checks across agencies to spot errors anywhere.

If you find an error (e.g., a payment marked late that was on time), you can file a dispute with the CRA. They must investigate and correct errors within 28 days. See article 14 for the full dispute process.

Practical Steps to Improve Your Credit Score

Improving your score takes time – typically 6 to 12 months of consistent behaviour. These steps work for most people:

Do these immediately:

- Register on the electoral roll at your current address.

- Check all three reports for errors and dispute any mistakes.

- Make sure you are not linked financially to someone with poor credit (e.g., a former joint account holder). You can file a notice of disassociation.

Do these over 3–6 months:

- Set up Direct Debits for minimum payments on all credit accounts – never miss a payment.

- Reduce credit utilisation below 30% by paying down balances or requesting a credit limit increase (without spending more).

- Keep old credit cards open, even if you do not use them.

- Space out credit applications – leave at least three months between applications.

Avoid these:

- Applying for multiple credit products in a short period.

- Using payday loans (these severely damage your score and signal financial distress).

- Maxing out credit cards.

- Closing old accounts unnecessarily.

How Long Do Negative Items Stay?

Understanding the timeline helps you plan. Most negative information disappears after six years:

- Missed payments – 6 years

- Defaults – 6 years

- CCJs – 6 years (or until paid, but the record remains)

- Bankruptcy – 6 years (or longer if restrictions remain)

- Hard searches – 12 months

After six years, the record vanishes completely. A default from 2018 will no longer appear in 2024. This is why time is one of the most powerful tools for credit repair.

Key Takeaways

- Check all three credit reports – errors are common and fixable.

- Payment history and credit utilisation matter most – never miss payments, keep utilisation below 30%.

- Register on the electoral roll – it is free and helps verification.

- Do not apply for multiple credit products quickly – space applications by three months.

- Negative records disappear after six years – focus on rebuilding, not worrying about the past.

This article is for general information and educational purposes only. It does not constitute financial advice. Tax rules, allowances, and product terms may change. Always check with HMRC or an FCA-authorised adviser for your personal circumstances.